Living paycheck to paycheck in the USA is exhausting. You work hard, pay your bills, and somehow end the month with nothing left over. Unexpected expenses throw your finances into chaos. You want to save money, build an emergency fund, and feel financially secure, but it feels impossible when your income barely covers basic needs. Rent keeps rising, groceries cost more every week, and gas prices fluctuate wildly. If you earn a low income in America, budgeting is not just helpful, it is essential for survival. But here is the truth that nobody talks about enough: you absolutely can budget on a low income in the USA and still save money. It will not be easy, and you will not save thousands of dollars immediately, but with the right strategy, even $50 or $100 per month adds up and creates a safety net that changes everything. This simple step-by-step guide will show you exactly how to budget with low income, cut unnecessary expenses, and start building financial stability no matter how much you earn.

The Problem With Budgeting on a Low Income

Budgeting on a low income in the USA comes with unique challenges that people with higher incomes simply do not face. Understanding these problems helps you create a realistic budget instead of following generic advice that does not apply to your situation.

High Rent and Housing Costs: Housing is the single biggest expense for most Americans, and it hits low-income earners especially hard. The standard financial advice says to spend no more than 30% of your income on rent. But in reality, many low-income Americans spend 40% to 60% or even more of their paycheck on rent because affordable housing is scarce. In cities like New York, Los Angeles, San Francisco, or even mid-sized cities like Denver or Austin, finding an apartment for under $1,200 per month is nearly impossible. If you earn $2,000 per month and your rent is $1,000, that is 50% of your income gone before you buy groceries, pay for transportation, or handle any other expense. This leaves very little room for savings or emergencies.

Inflation and Rising Costs: Everything is more expensive than it was a few years ago. Groceries, gas, utilities, insurance, and even basics like toothpaste and laundry detergent have all increased in price. When you are on a tight budget, a 20% increase in grocery costs or a $0.50 per gallon increase in gas prices is not a minor inconvenience, it is a major financial crisis. Low-income budgets have zero cushion for these kinds of increases, so inflation directly forces you to choose between needs. Do you buy less food, skip car maintenance, or cut back on utilities to make ends meet?

Debt and Credit Card Bills: Many low-income Americans carry credit card debt because credit cards become the emergency fund when unexpected expenses hit. Your car breaks down, your child needs new shoes, or you have a medical bill. Without savings, you put it on a credit card. Then you are stuck paying minimum payments with 20% to 25% interest rates, which means even a $1,000 balance costs you $200+ per year in interest alone. These debt payments eat up money that could go toward savings or essential needs, keeping you trapped in a cycle where you can never get ahead.

Irregular Expenses That Ruin Budgets: Traditional budgets focus on monthly expenses like rent, utilities, and food. But irregular expenses destroy low-income budgets. Car registration once a year, renters insurance every 6 months, back-to-school expenses in August, holiday spending in December, these costs are not monthly, but they are real and unavoidable. When you are living paycheck to paycheck with no savings, a $200 expense that only happens once a year can derail your entire financial plan for that month.

No Financial Cushion for Mistakes: Higher-income earners can absorb mistakes. They overspend one month and adjust the next month. But when you are on a low income, one mistake or unexpected expense can cascade into disaster. You overdraft your bank account ($35 fee), your electric bill is late ($25 late fee), you miss your car payment ($30 late fee), and suddenly you are $90 deeper in the hole. These fees and penalties make it even harder to recover.

Lack of Access to Financial Tools: Many low-income Americans do not have access to basic financial tools that make budgeting easier. Traditional banks require minimum balances that you cannot maintain, so you use check-cashing services that charge fees. You cannot get approved for low-interest loans, so you end up with payday loans at 300% to 400% APR. You do not have employer-sponsored retirement accounts or matching contributions. These systemic barriers make building wealth harder even when you are trying to budget perfectly.

The reality is that low income budgeting tips USA that work for someone earning $80,000 per year do not work when you are earning $25,000. You need a different approach that acknowledges your specific challenges and focuses on realistic, achievable goals.

Step-by-Step: How to Budget on a Low Income in the USA

Here is your practical, step-by-step plan for creating a monthly budget low income that actually works in real life.

Step 1 – Know Your Exact Monthly Income

Before you can create any budget, you need to know exactly how much money you have coming in every month. This sounds obvious, but many people skip this step or guess at their income, which makes budgeting impossible.

Focus on Net Income, Not Gross Income: Your gross income is what you earn before taxes and deductions. Your net income is what actually hits your bank account after taxes, Social Security, Medicare, health insurance, and any other deductions are taken out. Only your net income matters for budgeting because that is the money you actually have available to spend.

How to Calculate Monthly Net Income:

If you are paid weekly: Multiply your weekly paycheck by 4.33 (the average number of weeks per month). Example: $450 per week × 4.33 = $1,949 per month.

If you are paid bi-weekly (every 2 weeks): Multiply your paycheck by 2.17 (there are 26 pay periods per year, which equals 2.17 per month). Example: $900 every 2 weeks × 2.17 = $1,953 per month.

If you are paid twice per month (1st and 15th): Multiply your paycheck by 2. Example: $950 twice a month × 2 = $1,900 per month.

If you are paid monthly: That is your monthly income.

Track Variable Income: If your income varies (you work hourly with inconsistent hours, you get tips, you do gig work, or you have freelance income), calculate your average monthly income over the last 3 to 6 months. Add up your total income for the past 6 months and divide by 6. This gives you a realistic average to budget around. For budgeting purposes, always use your lowest earning month from the past 6 months as your baseline. This way you are prepared for down months and any extra income in good months can go straight to savings or debt payoff.

Include All Income Sources: List every source of money coming in: wages, tips, side gigs, government benefits (SNAP, WIC, unemployment, disability, Social Security), child support, alimony, etc. Do not leave anything out.

Example:

- Main job (bi-weekly): $800 × 2.17 = $1,736

- Weekend gig work: $150/month average

- Total monthly net income: $1,886

Write this number down at the top of your budget. This is your starting point. Every single expense you plan must fit within this number.

Step 2 – Track Every Expense (Even $5)

You cannot create an effective budget if you do not know where your money is actually going. Most people wildly underestimate how much they spend on small purchases that add up to hundreds of dollars per month.

Why Small Expenses Matter: A $5 coffee does not feel significant in the moment. But five coffees per week is $100 per month, $1,200 per year. A $12 lunch instead of packing food three times per week is $144 per month, $1,728 per year. These small decisions add up to massive amounts of money over time, especially when you are on a tight budget where every $20 matters.

How to Track Expenses:

Simple Notebook Method: Carry a small notebook or use the notes app on your phone. Every single time you spend money (cash, card, digital payment), write it down immediately. Include the date, what you bought, and how much it cost. Do this for one full month to get accurate data.

Bank Statement Method: If you use debit or credit cards for most purchases, review your bank and card statements for the past month. Categorize every transaction (rent, groceries, gas, eating out, subscriptions, etc.). This shows you exactly where your money went.

Budgeting Apps: Free apps like Mint, EveryDollar, YNAB (You Need A Budget), or Goodbudget automatically categorize your spending when you link your bank accounts. These apps do the tracking for you, which is easier than manual methods but requires you to trust the app with your financial data.

Cash Envelope System: If you prefer cash, withdraw your budgeted amount for each category and put it in labeled envelopes (groceries, gas, eating out, entertainment). When the envelope is empty, you stop spending in that category. This creates a physical, visual limit that is harder to ignore than numbers on a screen.

What to Track:

- Fixed expenses (rent, utilities, phone, internet, insurance, minimum debt payments)

- Variable expenses (groceries, gas, household items)

- Discretionary spending (eating out, entertainment, hobbies, subscriptions)

- Irregular expenses (car maintenance, medical co-pays, clothing, gifts)

- Every single purchase, no matter how small

The 30-Day Challenge: Track every expense for 30 days with brutal honesty. Do not change your spending behavior yet—just observe and record. At the end of the month, you will have a clear picture of where your money actually goes versus where you think it goes. Most people are shocked by what they discover.

Example of What You Might Find:

- Coffee shop: $87/month (thought it was $30)

- Food delivery apps: $156/month (thought it was $60)

- Subscriptions: $47/month (forgot about half of them)

- Gas station snacks and drinks: $64/month (did not track at all)

Total unnecessary spending: $354/month that could be redirected toward savings, debt, or essential needs.

Once you know where your money is going, you can make intentional decisions about where you want it to go instead.

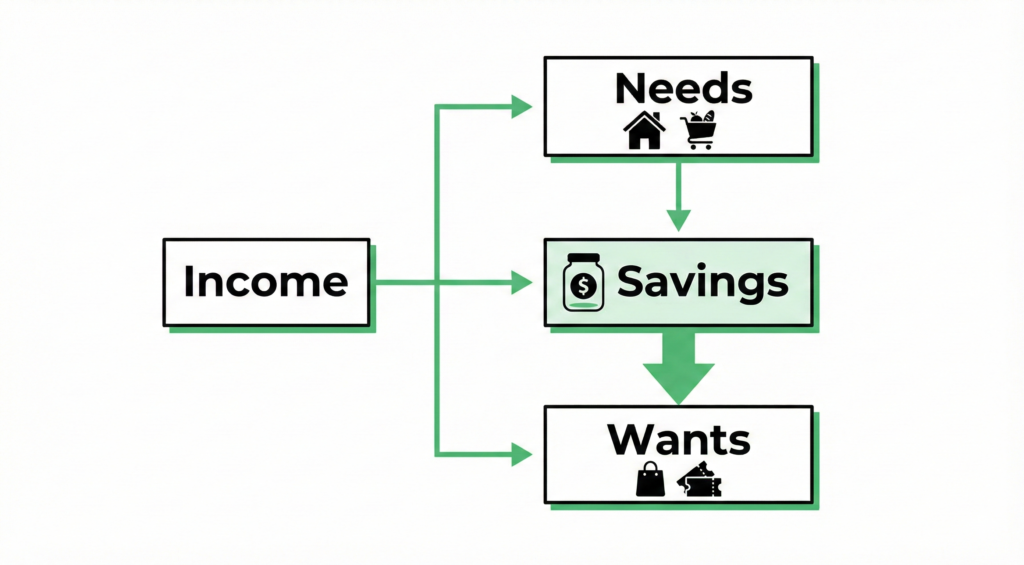

Step 3 – Use the 50-30-20 Rule (Modified for Low Income)

The traditional 50-30-20 budget rule says to spend 50% on needs, 30% on wants, and 20% on savings and debt. This works great for middle-income and high-income earners, but it is completely unrealistic for most people budgeting on a low income in the USA. Here is a modified version that actually works.

Modified Budget for Low Income: 70-20-10

70% on Needs (Essential Living Expenses): This covers rent, utilities, groceries, transportation, insurance, minimum debt payments, and other non-negotiable expenses. When you are on a low income, your needs often consume more than 50% of your income because housing and basic costs are not proportionally cheaper just because you earn less.

What counts as needs:

- Rent or mortgage

- Utilities (electric, gas, water, trash)

- Groceries (not eating out)

- Transportation (car payment, gas, bus/train pass, car insurance)

- Health insurance and essential medical care

- Phone (basic plan, not premium unlimited)

- Minimum payments on debts

- Childcare if you have children

20% on Bills and Debt Payments: This includes credit card payments above the minimum, student loans, car loans, and any other debt you are trying to pay off. If you have no debt, this category can be merged into savings.

10% on Savings and Emergency Fund: Yes, even if you earn a low income, you need to save something. Start with just 5% if 10% feels impossible. The goal is to build a small emergency fund of $500 to $1,000 as fast as possible. This prevents small emergencies from turning into financial disasters.

What About Wants?: You might notice there is no “wants” category in the modified 70-20-10 rule. That is because when you are truly on a low income, wants have to be minimized or eliminated temporarily until you build financial stability. This is not forever, but in the beginning stages of budgeting for beginners USA, you focus on survival and stability first, enjoyment second.

Realistic Example on $2,000/Month Income:

- Needs (70%): $1,400

- Debt payments (20%): $400

- Savings (10%): $200

If You Cannot Hit These Percentages: Many people on very low incomes cannot save 10% because their essential needs consume 80% to 90% of income. If that is you, start where you are. Save $25 or $50 per month. Something is better than nothing. As you cut expenses and possibly increase income, you can gradually increase your savings percentage.

Adjust Based on Your Reality: These percentages are guidelines, not rigid rules. If your rent alone is 60% of your income, you cannot force it to be 50%. Work with your actual numbers and do the best you can. The key is awareness and intentionality, not perfection.

Step 4 – Cut the “Silent Expenses”

Silent expenses are the costs you pay every month without thinking about them. They drain your budget slowly, like a leak you do not notice until the damage is done. Cutting these creates immediate breathing room in your budget without affecting your quality of life much.

Subscriptions You Forgot About: Streaming services, gym memberships, music apps, cloud storage, meal kit subscriptions, beauty boxes, gaming subscriptions—these add up fast. Go through your bank statements and list every subscription. Cancel anything you do not use at least once a week. Keep only the one or two you truly value.

Average savings: $30 to $100/month

Eating Out and Food Delivery: This is the biggest budget killer for most Americans. A $15 lunch instead of a packed sandwich five times per week is $300/month. A $35 DoorDash order twice a week is $280/month. These small conveniences add up to $500+ per month for many people.

Cut this by 75%: Pack lunch for work, cook dinner at home, make coffee at home, and save eating out for special occasions only (once or twice per month).

Average savings: $200 to $400/month

Convenience Store and Gas Station Purchases: Stopping for a drink, snacks, or lottery tickets at gas stations or convenience stores is expensive. A $3 energy drink every morning is $90/month. Buy these items in bulk at grocery stores or Walmart instead.

Average savings: $40 to $80/month

Unused Gym Memberships: If you are paying $30 to $60/month for a gym you never go to, cancel it. Use free YouTube workout videos, walk or run outside, or do bodyweight exercises at home.

Average savings: $30 to $60/month

Cable TV: If you are still paying for cable, cut it. Use a digital antenna for free local channels and one or two streaming services instead of cable’s $80 to $150/month cost.

Average savings: $50 to $120/month

Bank Fees: Overdraft fees, monthly maintenance fees, ATM fees, and paper statement fees can add up to $20 to $50/month. Switch to a free checking account at an online bank or credit union. Use your bank’s ATMs to avoid fees.

Average savings: $20 to $50/month

Phone Plan Downgrades: If you are paying $70 to $100/month for unlimited everything, consider switching to a budget carrier like Mint Mobile, Cricket, or Visible. You can get perfectly good service for $25 to $40/month.

Average savings: $30 to $60/month

Car-Related Waste: Premium gas when regular works fine, car washes every week, expensive oil changes at the dealership instead of a local shop—these add up. Buy gas at the cheapest stations (use GasBuddy app), wash your car at home, and find affordable local mechanics instead of dealerships.

Average savings: $30 to $50/month

Total Potential Savings from Cutting Silent Expenses: $430 to $920/month

Even cutting half of these silent expenses can free up $200 to $400/month that can go toward building an emergency fund, paying off debt, or covering essential needs without stress.

Step 5 – Build a Mini Emergency Fund ($500 First)

One of the biggest reasons people on low incomes stay stuck financially is the lack of an emergency fund. Without savings, every unexpected expense becomes a crisis that requires credit cards, payday loans, or borrowing from family, which creates more financial stress and debt.

Why $500 Is Your First Goal: A $500 emergency fund will not cover every possible emergency, but it will cover most of the common ones that destroy low-income budgets:

- Car repair: $300 to $500

- Medical co-pay or urgent care visit: $50 to $150

- Broken phone that needs replacing: $100 to $200

- Overdraft fees and late payment fees: $35 to $75

- Minor home repair (leaking pipe, broken appliance): $100 to $300

Having $500 in savings means these common emergencies do not force you into credit card debt or payday loans. You handle them with cash and move on with your life.

How to Save $500 on a Low Income:

Save $25/month: Reach $500 in 20 months (1 year and 8 months)

Save $50/month: Reach $500 in 10 months

Save $100/month: Reach $500 in 5 months

Pick the number that fits your budget after cutting silent expenses. Even $25/month is progress.

Automatic Transfers: Set up an automatic transfer from your checking account to a savings account the day after payday. Even $10 or $20 per paycheck adds up. Make it automatic so you do not have to think about it or be tempted to skip it.

Use Windfalls: Any unexpected money (tax refund, work bonus, birthday money, sold items, overtime pay) goes directly to your emergency fund until you hit $500. Do not spend it.

Round-Up Savings Apps: Apps like Acorns, Qapital, or Chime round up your purchases to the nearest dollar and save the difference. Buying coffee for $3.50 rounds up to $4.00 and saves $0.50. These small amounts add up to $20 to $40/month without you noticing.

Where to Keep Your Emergency Fund: Put it in a separate savings account that is not linked to your debit card. This creates a barrier between you and impulse spending. Online high-yield savings accounts from banks like Ally, Marcus, or Discover offer better interest rates than traditional banks and make the money slightly harder to access (good for preventing impulse withdrawals).

After You Hit $500: Your next goal is $1,000, then 1 month of expenses, then 3 months of expenses. But focus on $500 first. That first milestone changes everything psychologically and financially.

Building credit and managing money go hand in hand. If you are starting from scratch financially, learn how to build credit with no credit history in the USA to improve your financial options while you budget and save.

Example Monthly Budget (Low Income – USA)

Here is a realistic example of a monthly budget for someone earning a low income in the USA. This shows you exactly how to allocate every dollar.

Total Monthly Net Income: $2,200

Essential Needs (70% = $1,540):

- Rent (including utilities): $900

- Groceries: $300

- Transportation (car payment, insurance, gas): $250

- Phone: $35

- Health insurance (not covered by employer): $0 (Medicaid)

- Basic household items: $55

Total Needs: $1,540

Debt Payments (20% = $440):

- Credit card minimum payments: $150

- Student loan payment: $100

- Car loan payment (included in transportation above): $0

- Extra toward highest-interest debt: $190

Total Debt Payments: $440

Savings and Emergency Fund (10% = $220):

- Emergency fund: $150

- Future irregular expenses (car registration, gifts, etc.): $70

Total Savings: $220

Grand Total: $1,540 + $440 + $220 = $2,200 (exactly matches income)

Notes on This Budget:

- No money allocated to eating out, entertainment, or wants—this is survival mode budgeting while building stability

- Once the emergency fund hits $500 to $1,000, some of that $150/month can shift to debt payoff or allow for small discretionary spending

- The $70 set aside for irregular expenses prevents future budget emergencies when car registration or holiday gifts come due

- This person is aggressively paying down debt while also building savings, which is the balanced approach

If Your Income Is Even Lower ($1,500/month example):

Total Monthly Net Income: $1,500

Essential Needs (80% = $1,200):

- Rent with roommate: $600

- Groceries: $250

- Transportation (bus pass + occasional rideshare): $100

- Phone: $25

- Health insurance: $0 (Medicaid)

- Household items: $225

Total Needs: $1,200

Debt Payments (15% = $225):

- Credit card minimum payments: $225

Total Debt: $225

Savings (5% = $75):

- Emergency fund: $50

- Irregular expenses fund: $25

Total Savings: $75

Notes on Lower Income Budget:

- Percentage shifted to 80-15-5 because needs consume more at very low incomes

- Still saving something ($50/month = $600/year = meaningful emergency fund in 1 year)

- Living with a roommate cuts rent in half

- Using public transportation instead of car ownership saves hundreds per month

- Once emergency fund is built, that $50 can shift to debt payoff or wants

The key is adapting the percentages to your reality while maintaining the principle: track everything, cut unnecessary expenses, pay minimums on debt, and save something every month.

Common Budgeting Mistakes to Avoid

Even with the best intentions, people make these mistakes that sabotage their low-income budgets.

Setting Unrealistic Saving Goals: You see advice online saying “save 20% of your income” or “build a 6-month emergency fund immediately.” When you earn $1,800/month and your rent alone is $950, saving 20% ($360/month) is mathematically impossible. Trying to hit unrealistic goals leads to frustration and giving up entirely. Instead, save what you actually can, even if it is just $25 or $50 per month. Small, consistent progress beats ambitious goals that you abandon after two weeks.

Forgetting About Irregular Expenses: Most budgets only account for monthly bills, but irregular expenses destroy budgets every single time. Car registration, renters insurance, holiday gifts, back-to-school costs, annual subscriptions—these expenses are not monthly, but they are 100% guaranteed to happen. Create a sinking fund where you set aside money every month for these irregular costs. Add up all your irregular expenses for the year, divide by 12, and save that amount monthly. Example: $600 in annual irregular expenses ÷ 12 = $50/month saved for these costs.

Not Tracking Cash Spending: You carefully track your debit card purchases but pull out $40 cash from the ATM and spend it on random things without tracking. Cash disappears faster than digital payments because it is harder to track. Either track cash purchases just as carefully as card purchases, or avoid using cash entirely and put everything on a debit card so it is all recorded.

Lifestyle Inflation on Tiny Raises: You get a $0.50/hour raise or start earning $100 more per month. Instead of putting that extra money toward savings or debt, you immediately increase your spending by eating out more or upgrading your phone plan. This keeps you stuck at the same financial level forever. When income increases, maintain your current spending level and put 100% of the increase toward financial goals until you hit stability (emergency fund + manageable debt).

Comparing Yourself to Others: Your friend posts Instagram photos from vacation, drives a nice car, and always has new clothes. You feel bad about your strict budget and give up, thinking it is pointless. Remember that most people are in debt funding lifestyles they cannot afford. Your friend might have $15,000 in credit card debt and zero savings. Stay focused on your own path. Comparison kills financial progress.

Budgeting for Perfection Instead of Progress: You create a perfect budget spreadsheet with color-coded categories and detailed formulas, then abandon it after one month because you overspent by $30 on groceries and feel like you failed. Budgeting is not about perfection. It is about awareness and making better decisions over time. If you go over budget in one category, adjust somewhere else. Keep going. Progress matters, not perfection.

Not Having a Buffer: Life is unpredictable. You will have months where you overspend or unexpected costs arise. Build a small buffer into your budget if possible (even $20 to $50 of “unallocated” money) so minor surprises do not derail everything. This prevents the all-or-nothing mentality where one mistake makes you give up entirely.

FAQs

Can you really save money on a low income in the USA?

Yes, you absolutely can save money on a low income in the USA, but it requires cutting expenses aggressively and starting with small, realistic goals.

The key is to start where you are, not where you wish you were. If you can only save $25 per month, that is $300 per year, which is enough to cover many minor emergencies that would otherwise go on a credit card. If you can save $50 per month, that is $600 per year, which builds a meaningful emergency fund in 12 months.

How to save on low income:

- Cut silent expenses (subscriptions, eating out, convenience purchases)

- Use generic brands instead of name brands at the grocery store

- Eliminate one major expense (cable TV, unused gym, expensive phone plan)

- Put any windfalls (tax refunds, bonuses, gift money) directly into savings

- Automate savings so it happens before you have a chance to spend the money

Realistic savings timeline:

- Save $25/month = $300/year

- Save $50/month = $600/year

- Save $100/month = $1,200/year

These might seem like small amounts compared to advice that says “save 6 months of expenses,” but they are life-changing amounts when you are living paycheck to paycheck. A $300 emergency fund prevents one car repair from becoming a financial disaster.

The biggest lie about saving money is that it is only possible if you have a high income. The truth is that saving is about spending less than you earn, regardless of the amount. Someone earning $2,000/month who saves $100 is doing better financially than someone earning $5,000/month who saves nothing.

What is the best budgeting method for low income earners?

The best budgeting method for low-income earners is either zero-based budgeting or the modified 50-30-20 rule (adjusted to 70-20-10 for low incomes).

Zero-Based Budgeting: This method assigns every single dollar a job before the month begins. Your income minus all your planned expenses and savings should equal exactly zero. This ensures you are intentional with every dollar and nothing slips through the cracks.

How it works:

- List your total monthly income

- List all expenses (fixed, variable, savings, debt)

- Subtract expenses from income

- If there is money left over, assign it to a category (extra debt payment, savings, or discretionary)

- Keep adjusting until income minus expenses equals zero

Zero-based budgeting works well for low incomes because it forces you to account for every dollar, which prevents waste.

Modified 70-20-10 Rule: This method splits your income into three categories: 70% for essential needs, 20% for debt payments, and 10% for savings. It is simpler than zero-based budgeting and still creates structure without being overwhelming.

Cash Envelope System: This is another excellent method for low-income earners. You withdraw your budgeted amounts in cash and put them in labeled envelopes (groceries, gas, entertainment). When the envelope is empty, you stop spending in that category. This creates a physical, visual limit that is harder to ignore than a number on a spreadsheet.

The best method is the one you will actually stick with for more than one month. If detailed spreadsheets stress you out, use the envelope system. If you like data and tracking, use zero-based budgeting. Experiment and find what works for your personality and lifestyle.

Should I use credit cards if my income is low?

You can use credit cards responsibly on a low income, but only if you pay the full balance every month and keep your credit utilization under 30%.

When credit cards help on low income:

- Building credit history (which helps you qualify for better rates on loans and apartments)

- Earning cash back or rewards on purchases you would make anyway

- Fraud protection (credit cards offer better protection than debit cards)

- Emergency backup (only for true emergencies, not regular spending)

When credit cards hurt on low income:

- When you carry a balance month to month and pay 18% to 25% interest

- When you use them to fund a lifestyle you cannot afford

- When they enable overspending beyond your budget

- When you max them out, creating high utilization that damages your credit score

Safe Credit Card Use on Low Income:

- Only use credit cards for budgeted purchases you already planned to make

- Pay the full balance every month before the due date to avoid interest

- Set up autopay for at least the minimum payment as a safety net

- Keep utilization under 30% of your credit limit (under 10% is ideal)

- Track credit card spending in your budget just like cash or debit purchases

If you cannot trust yourself to follow these rules, avoid credit cards entirely and use a debit card or cash until you have better spending discipline and a solid emergency fund.

Credit utilization is a critical factor if you do use credit cards. Make sure you understand what credit utilization ratio is and how it affects your credit score in the USA so you use credit cards strategically without damaging your credit.

Conclusion

Learning how to budget on a low income in the USA is not about earning more money—it is about controlling what you already earn and making every dollar count. You will not save thousands of dollars overnight, and you will not eliminate all financial stress immediately. But by tracking your expenses, cutting silent costs, following a realistic budget structure, and saving even $25 to $50 per month, you create stability and break the paycheck-to-paycheck cycle.

The budgeting strategies in this guide work because they are designed for real low-income situations in America, not generic advice that assumes you have money left over at the end of the month. Start with step one today: calculate your exact monthly net income. Then track your spending for 30 days. Once you know where your money is going, you can take control and redirect it toward your priorities instead of letting it disappear into random purchases.

Your next step: Create your first budget this week. Use the 70-20-10 rule, zero-based budgeting, or the cash envelope system—whichever feels manageable. Set a small savings goal ($500 emergency fund) and work toward it $25 or $50 at a time. In 12 months, you will look back and be amazed at what you built with discipline and consistency.

Budgeting is not about deprivation or never enjoying life. It is about making conscious choices so you can afford the things that truly matter while building financial security. Start today. Your future self will thank you.