Starting your financial life in the USA without any credit history feels like being trapped in an impossible situation. Banks will not give you a credit card because you have no credit history, but you cannot build credit history without a credit card. Landlords reject your rental applications, utility companies demand huge security deposits, and even getting a phone plan becomes complicated. Whether you are a new immigrant, an international student, or a young American who has never used credit before, the challenge is real. But here is the good news: you absolutely can build credit with no credit history. It just requires knowing the right steps and being willing to start small. This beginner’s guide will show you exactly how to establish credit from scratch in the USA, step by step, using proven strategies that actually work.

Building Credit From Scratch in the USA

In the United States, your credit history is one of the most important numbers in your financial life. It determines whether you can rent an apartment, get approved for loans, qualify for credit cards, and even affects your insurance rates and job prospects in some industries.

For people who are new to the country or have simply never used credit before, this creates a frustrating catch-22 situation. You need credit to get credit. Banks and lenders want to see a track record of responsible borrowing before they trust you with a credit card or loan. But how are you supposed to create that track record when no one will approve you in the first place?

This problem affects millions of people in the USA every year. New immigrants arrive with excellent financial histories in their home countries, only to discover those records mean nothing here. International students on F-1 or J-1 visas struggle to get basic financial services. Young Americans who were taught to avoid debt and only use cash find themselves penalized for being financially responsible.

The traditional financial system was not designed for people starting from zero. It favors those who already have established credit. But the good news is that you can build credit even with zero history. Financial institutions have created products specifically designed for people in your situation, and if you use them strategically, you can go from no credit history to a good credit score in as little as 6 to 12 months.

This guide will walk you through every step of building credit from scratch, from opening your first secured credit card to establishing a solid credit score that opens doors throughout the American financial system.

Why Having No Credit History Is a Problem

Before we dive into solutions, you need to understand exactly how having no credit history affects your life in the USA. The impact goes far beyond just credit cards.

Credit Card Rejections: When you apply for a standard credit card with no credit history, you will almost certainly be denied. Banks use your credit score and credit report to assess risk. With no history, they have no data to evaluate, so they default to rejection. This means you cannot access the convenience and security of credit cards, you miss out on fraud protection that debit cards lack, and you cannot earn rewards or build credit through normal spending.

Loan Denials: Trying to get an auto loan, personal loan, or mortgage with no credit history is nearly impossible. Even if a lender is willing to work with you, they will charge extremely high interest rates to compensate for the perceived risk. A car loan that would cost someone with good credit 5% APR might cost you 15% to 20% APR, or you might be denied entirely. Student loans are an exception because federal student loans do not require credit checks, but private student loans absolutely do.

High Security Deposits: Utility companies (electricity, gas, water, internet) often check credit before setting up service. With no credit history, they see you as a risk and require massive security deposits, sometimes $200 to $500 or more, just to turn on your electricity or internet. The same applies to phone carriers. Want a new iPhone with a monthly payment plan? Not without credit history. You will have to pay full price upfront or settle for a prepaid plan.

Rental Application Rejections: Landlords in competitive rental markets heavily rely on credit checks. No credit history often equals no apartment, especially in major cities like New York, San Francisco, or Los Angeles. Even if a landlord is willing to rent to you, they will likely require a co-signer (someone with good credit who agrees to be responsible if you do not pay) or demand 3 to 6 months of rent upfront as security. This locks up thousands of dollars that you could use for other expenses.

Higher Insurance Premiums: In most states, insurance companies use credit-based insurance scores to set your auto and home insurance rates. No credit history means higher premiums, sometimes 20% to 50% more expensive than someone with good credit would pay for the exact same coverage.

Employment Challenges: Certain jobs, particularly in finance, government, or positions requiring security clearance, include credit checks as part of the background screening process. While they cannot see your credit score, they can see your credit report. Having no credit history might not disqualify you, but it raises questions and could put you at a disadvantage compared to other candidates.

No Financial Safety Net: Perhaps the most dangerous aspect of having no credit is that you have no access to emergency credit when you need it most. If your car breaks down, you face a medical emergency, or you lose your job, people with credit cards or personal loan access have options. Without credit history, you are forced to rely entirely on cash savings, which many people do not have.

The longer you wait to start building credit, the longer you remain locked out of these basic financial services. The good news is that building credit is not complicated once you know the right steps.

Start With a Secured Credit Card

A secured credit card is the single best tool for building credit with no credit history. It is specifically designed for people in your exact situation.

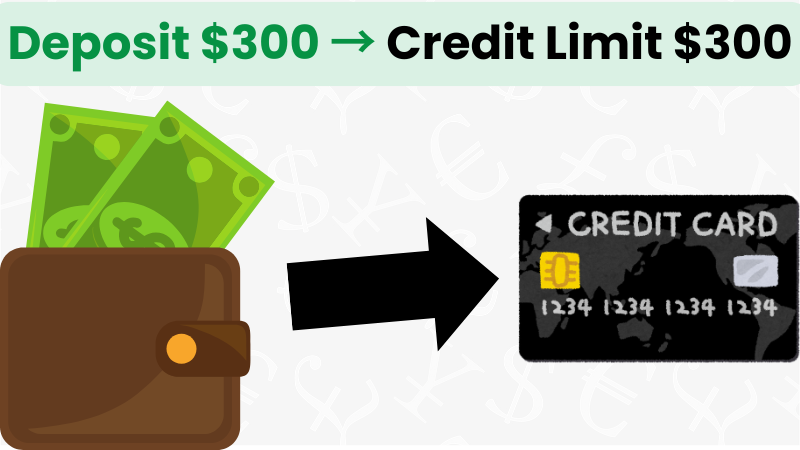

What Is a Secured Credit Card?: A secured credit card works almost identically to a regular credit card, with one key difference: you put down a cash deposit that serves as collateral. This deposit protects the bank if you fail to pay your bill, which is why they are willing to approve people with no credit history.

How It Works: You open a secured card and deposit anywhere from $200 to $500 (sometimes more) with the credit card company. This deposit becomes your credit limit. For example, if you deposit $300, you get a $300 credit limit. You can then use the card just like any other credit card to make purchases, and you pay your bill every month. As long as you pay on time, your deposit sits safely in an account and you get it back when you close the card or upgrade to an unsecured card.

It Reports to Credit Bureaus: This is the crucial part. Secured credit cards report your payment activity to all three major credit bureaus (Experian, Equifax, and TransUnion) just like regular credit cards. Every on-time payment you make builds positive credit history. Within 6 months of responsible use, you will have established a credit score.

Best Secured Credit Cards for Beginners:

- Discover it Secured: No annual fee, cash back rewards, and Discover automatically reviews your account to see if you qualify for an unsupRegular upgrade

- Capital One Platinum Secured: Possible to get a higher credit limit than your deposit, no annual fee

- Citi Secured Mastercard: Reports to all three bureaus, no annual fee

How to Use Your Secured Card Strategically:

- Use it for small, regular purchases (gas, groceries, subscriptions)

- Pay your balance in full every month before the due date to avoid interest

- Keep your balance below 30% of your limit (ideally under 10%)

- Set up autopay for at least the minimum payment to never miss a due date

- After 6 to 12 months of on-time payments, request an upgrade to an unsecured card and get your deposit back

Common Concerns:

“Is a secured card the same as a prepaid card?” No. Prepaid cards do not build credit because you are just spending your own money. Secured cards are real credit cards that report to bureaus.

“Will people know I have a secured card?” No. The card looks identical to a regular credit card, and merchants cannot tell the difference.

“What if I cannot afford a $300 deposit?” Some secured cards allow deposits as low as $200. Start there and work your way up as you can afford it.

A secured credit card is your foundation. It is the first step that makes all other credit-building strategies possible.

Become an Authorized User

Becoming an authorized user on someone else’s credit card is one of the fastest ways to build credit with no credit history, but it requires having someone who trusts you and has good credit.

What Is an Authorized User?: When someone adds you as an authorized user on their credit card account, you get a card with your name on it that is linked to their account. The account’s full payment history, age, and credit limit may appear on your credit report, instantly giving you credit history.

How It Helps Build Credit: If the primary cardholder has a long history of on-time payments, low utilization, and an old account, all of that positive history can be added to your credit report. This can create an immediate boost to your credit score and give you the credit history you need to qualify for your own cards.

Who to Ask: The ideal person to ask is:

- A parent, spouse, or sibling with excellent credit

- Someone who has had their card for at least 2 to 5 years

- Someone with perfect payment history (no late payments)

- Someone who keeps their balance low (under 30% utilization)

- Someone you trust and who trusts you

Set Clear Expectations: When asking someone to add you as an authorized user, be completely transparent about your intentions. Explain that you are trying to build credit and that you do not need to actually use the card. In most cases, the primary cardholder can add you to the account, keep your card locked away, and you still benefit from the credit history without ever making a purchase.

The Risks (Be Honest About These):

For you: If the primary cardholder misses payments, maxes out the card, or gets into financial trouble after adding you, those negative marks will also appear on your credit report and hurt your score.

For them: Anything you charge on the card is their legal responsibility to pay. If you run up charges and do not pay them back, it is their credit and finances on the line.

Best Practices:

- Only become an authorized user on accounts with perfect payment history

- Confirm with the credit card issuer that they report authorized users to all three credit bureaus (not all do)

- Consider not using the card at all, or only using it for agreed-upon small purchases that you immediately pay back

- Stay in regular communication with the primary cardholder about the account status

Timeline: Once added as an authorized user, the account typically appears on your credit report within 30 to 60 days. If the account is old and in good standing, you might see an immediate credit score boost of 20 to 100+ points.

Important Note: Becoming an authorized user alone is not enough to build strong credit long-term. You also need your own credit accounts (like a secured card) to show you can manage credit independently.

Use Credit Builder Loans

Credit builder loans are a unique financial product designed specifically for people trying to build credit with no credit history. They work backward compared to traditional loans.

What Is a Credit Builder Loan?: Instead of receiving money upfront and paying it back (like a normal loan), with a credit builder loan you make monthly payments into a savings account held by the lender. Once you have made all the payments, you get access to the money. Meanwhile, your payments are reported to the credit bureaus, building your credit history.

How It Works Step-by-Step:

- You apply for a credit builder loan (usually $300 to $1,000)

- The lender approves you (these loans are easy to get approved for because there is minimal risk to the lender)

- The loan amount is placed in a locked savings account that you cannot access yet

- You make monthly payments (usually $25 to $100) for 6 to 24 months

- Each payment is reported to the credit bureaus as on-time loan payment

- After making all payments, you get the full amount back minus a small fee or interest

- You now have 6 to 24 months of positive payment history on your credit report

Where to Get Credit Builder Loans:

- Local credit unions (often have the best terms and lowest fees)

- Community banks

- Online lenders like Self, Credit Strong, or MoneyLion

- Some nonprofits and community development financial institutions (CDFIs)

Benefits:

- Easy approval even with no credit history

- Builds payment history (35% of your credit score)

- Forces you to save money while building credit

- Usually reports to all three credit bureaus

- Low monthly payments fit most budgets

Costs and Fees:

- Interest rates: 6% to 16% APR typically

- Administrative fees: $0 to $15 depending on the lender

- The total cost is usually $20 to $50 for a 12-month loan

Example: You take out a $600 credit builder loan with a 12-month term. Your monthly payment is $52. After 12 months, you have paid $624 total ($24 in interest and fees). You receive $600 back. You paid $24 to build 12 months of positive credit history, which is a good deal.

Strategic Use: Combine a credit builder loan with a secured credit card for maximum impact. The loan shows you can handle installment debt (like auto loans or mortgages), while the secured card shows you can manage revolving credit (credit cards). Having both types of credit in your history makes your credit profile stronger.

Important: Never miss a payment on a credit builder loan. The entire purpose is to build positive payment history. One missed payment defeats the purpose and damages the credit you are trying to build.

Always Pay Bills on Time

Payment history is the single most important factor in your credit score, accounting for 35% of your FICO score. Nothing matters more than paying every bill on time, every single month, without exception.

Why Payment History Matters So Much: Lenders care about one thing above all else: will you pay them back? Your payment history is the best predictor they have. Someone who has never missed a payment in 5 years is a much safer bet than someone with multiple late payments, even if everything else about their credit profile is identical.

What Counts as On-Time: A payment is considered on-time if the credit card company or lender receives it by the due date shown on your statement. Most companies give you until 5pm in their time zone on the due date. After that, it is late.

Grace Period vs. Late Reporting: There is an important distinction. If you pay 1 day late, you will be charged a late fee (usually $25 to $40), but it will not be reported to the credit bureaus. Credit card companies only report late payments to the bureaus after you are 30 days past due. However, you should never rely on this grace period. Aim to pay before the due date, every time.

How to Ensure You Never Miss a Payment:

Set Up Autopay: Log into every credit account and set up automatic payments for at least the minimum amount due. This is your safety net. Even if you forget, lose track of time, or are traveling, autopay ensures you stay current.

Pay More Than the Minimum: While autopay should be set for the minimum, try to manually pay more (ideally the full balance) before the due date. This keeps your utilization low and saves you money on interest.

Use Calendar Reminders: Set phone alerts for 5 days before each due date. This gives you time to check that autopay is set up correctly and to make additional payments if needed.

Link to Checking Account: Make sure your autopay is linked to a checking account that always has enough money to cover the minimum payment. An autopay that fails due to insufficient funds is just as bad as not paying at all.

Check Weekly: Once a week, quickly log into your credit accounts to verify everything is running smoothly. This takes 5 minutes and catches any issues before they become problems.

The Cost of One Late Payment: Missing a payment by 30+ days can drop your credit score by 60 to 110 points and stays on your credit report for 7 years. When you are building credit from scratch, you cannot afford even one mistake. Your goal is a perfect payment history from day one.

Non-Credit Bills: While most utility bills, rent, and phone bills do not report to credit bureaus when you pay on time, they absolutely will report if you go to collections. Pay everything on time to avoid surprises.

Building credit requires discipline and consistency. Paying on time is the foundation that everything else is built on.

Keep Credit Utilization Low

Credit utilization is the second most important factor in your credit score (30% of your FICO score), and managing it correctly is crucial when you are building credit from scratch.

What Is Credit Utilization?: Credit utilization is the percentage of your available credit that you are currently using. It is calculated by dividing your total credit card balances by your total credit limits.

Formula: (Total Balances ÷ Total Credit Limits) × 100 = Utilization Percentage

Why It Matters: Lenders see high utilization as a sign of financial stress. If you are using 80% to 90% of your available credit, it suggests you are living beyond your means and might be close to defaulting. Low utilization (under 30%, ideally under 10%) signals that you have your finances under control and are not desperate for credit.

Target Numbers:

- Keep overall utilization under 30% (acceptable)

- Aim for under 10% (ideal for building strong credit)

- Never max out your cards, even temporarily

Example: You have a secured credit card with a $300 limit. To keep utilization under 30%, your balance should never exceed $90. To optimize your score, keep it under $30 (10% utilization).

How to Keep Utilization Low When Building Credit:

Use Your Card for Small Purchases: Put one or two recurring bills on your card (Netflix, Spotify, gym membership) and set up autopay to pay the balance in full each month. This shows usage without high balances.

Pay Multiple Times Per Month: Instead of waiting for your due date, make payments every week or even after every purchase. This keeps your balance consistently low.

Pay Before Statement Closing Date: Your credit card company reports your balance to the credit bureaus on your statement closing date (not your due date). If you pay down your balance a few days before your statement closes, the lower balance is what gets reported.

Request Credit Limit Increases: After 6 to 12 months of responsible use, call your credit card company and request a credit limit increase. If your limit goes from $300 to $500, your utilization automatically drops even if your spending stays the same.

Do Not Close Your First Card: Even if you upgrade to better cards later, keep your first secured card open (after it converts to unsecured). The available credit helps keep your overall utilization low.

Credit utilization plays a huge role in building credit, so make sure you understand what credit utilization ratio is and how it affects your credit score in the USA.

Common Mistake to Avoid: Some people think they need to carry a balance and pay interest to build credit. This is completely false. You can use your card, pay it off in full every month (zero interest), and still build excellent credit. In fact, paying in full is better because it keeps your utilization at or near 0%.

The Impact on Your Score: Going from 80% utilization to 20% utilization can boost your score by 40 to 80 points. When you are building credit from scratch, managing utilization correctly from the beginning sets you up for success.

Example of Building Credit From Zero

Let’s walk through a realistic example of someone building credit with no credit history in the USA.

Meet Maria from Colombia:

- Age: 25

- Situation: Moved to the USA on an H-1B work visa

- Credit history: Zero (excellent credit in Colombia, but that does not transfer)

- Income: $55,000/year

- Goal: Build credit to eventually buy a car and rent an apartment without a co-signer

Month 1 – Maria Takes Action:

Maria applies for a secured credit card through Discover. She deposits $300 and receives a $300 credit limit. She is approved instantly despite having no US credit history because it is a secured card.

She also asks her American roommate (who has had a credit card for 6 years with perfect payment history) to add her as an authorized user. Her roommate agrees, and Maria promises not to use the card.

Month 2 – First Payments:

Maria puts her Spotify subscription ($10/month) and gym membership ($30/month) on her secured card. She sets up autopay to pay the full balance every month.

She also opens a $500 credit builder loan through her local credit union with a 12-month term. Her monthly payment is $43.

Total monthly credit-building cost: $40 in charges (which she pays off) + $43 loan payment = $83/month

Month 3 – Building History:

Maria makes all payments on time. Her authorized user account from her roommate appears on her credit report, giving her instant credit history from a 6-year-old account.

Month 6 – First Credit Score:

After 6 months of perfect payment history, Maria checks her credit score for the first time. She has a 680 credit score.

Her credit report shows:

- Secured credit card: 6 months of perfect payments, 13% average utilization

- Authorized user account: 6+ years of history (borrowed from roommate’s account)

- Credit builder loan: 6 months of on-time payments

Month 12 – Upgrades and Progress:

Maria’s credit builder loan is complete. She gets her $500 back minus $30 in fees.

She applies for her first unsecured credit card (Capital One Quicksilver) and is approved with a $2,000 credit limit because she now has 12 months of proven credit history and a 710 credit score.

Discover reviews her secured card and graduates her to an unsecured card, returning her $300 deposit.

Month 18 – Financial Freedom:

Maria’s credit score is now 730. She applies for an auto loan and is approved with a 6.5% interest rate (compared to 15%+ she would have faced with no credit history).

She rents a new apartment without needing a co-signer and gets approved for a premium rewards credit card.

What Made This Work:

- Started with the right tools (secured card + authorized user + credit builder loan)

- Paid every bill on time without exception

- Kept credit utilization under 30% (usually under 15%)

- Never applied for too much credit at once

- Stayed patient and consistent for 18 months

Maria’s journey from zero credit to a 730 score in 18 months is realistic and achievable for anyone willing to follow the same steps.

Common Mistakes to Avoid When Building Credit

Even people who understand the basics of building credit make these critical mistakes that slow their progress or damage their scores.

Applying for Too Many Credit Cards at Once: When you have no credit history, it is tempting to apply for multiple cards hoping one will approve you. This is a mistake. Every application creates a hard inquiry on your credit report (even if you are denied), and multiple inquiries in a short period make you look desperate and lower your score by 10 to 30 points. Instead, research which cards are designed for people with no credit history (secured cards, student cards) and apply for one at a time.

Maxing Out Your First Credit Card: Your first secured card probably has a low limit (like $300). Some people immediately max it out, thinking they need to “use” their credit. This creates 100% utilization, which tanks your score even if you pay on time. Keep your balance under 30% of your limit, ideally under 10%, and pay it off in full every month.

Missing Payments Because “It Is Just One Time”: When you are building credit from zero, you have no cushion. People with established credit can sometimes recover from one late payment (though it still hurts). But when you have only 3 or 6 months of credit history, one late payment can drop your score by 100+ points and label you as high-risk before you even get started. There is no room for “just this once” when building credit. Set up autopay and never miss a payment.

Closing Your First Credit Card Too Early: After 12 months, many secured cards convert to unsecured cards and return your deposit. Some people immediately close the account because they have “better” cards now. This is a mistake because:

- You lose the available credit, increasing your utilization on other cards

- You lose your oldest account, which shortens your credit history

- You remove a card with perfect payment history from your active accounts

Keep your first card open. Use it for one small recurring charge and set it to autopay. This maintains your credit history and keeps your utilization low.

Using Credit Builder Loans and Then Missing Payments: The entire point of a credit builder loan is to build positive payment history. If you miss payments on this loan, you are paying fees to damage your credit. It defeats the purpose completely. If you cannot afford the $25 to $50 monthly payment on a credit builder loan, do not take it out until you can.

Believing “Credit Repair” Scams: Companies that promise to “fix your credit instantly” or “remove anything from your credit report legally” are scams. When you have no credit history, you have nothing to repair. You need to build credit, which takes time and responsible behavior. Do not waste money on these services.

Ignoring Credit Reports: Some people start building credit but never check their credit reports to verify everything is being reported correctly. Mistakes happen. Your secured card might not be reporting to all three bureaus. Your authorized user account might not have appeared. Check your credit reports every 3 months (you can get free reports from each bureau once per year at AnnualCreditReport.com) to ensure your hard work is actually showing up.

Comparing Your Progress to Others: Someone might tell you they went from no credit to a 750 score in 6 months. Your score might be 650 after the same time period. Do not get discouraged. Credit scores depend on many factors including the age of your accounts, how much credit you have, and more. Focus on your own journey, not someone else’s timeline.

Avoiding these mistakes keeps you on track to build strong credit as quickly as possible.

FAQs About Building Credit With No History

How long does it take to build credit in the USA?

Most people can establish a credit score within 3 to 6 months of opening their first credit account, but building good credit (670+) typically takes 6 to 12 months of responsible credit use.

Here is a realistic timeline:

Month 1 to 3: You open a secured credit card and possibly become an authorized user. You are making payments, but you might not have a credit score yet because you need at least 3 months of credit history for FICO to generate a score.

Month 3 to 6: Your first credit score appears, usually in the 580 to 650 range if you have been paying on time and keeping utilization low. This is considered “fair” credit.

Month 6 to 12: With continued on-time payments, low utilization, and possibly adding a credit builder loan or another credit card, your score climbs into the “good” range (670 to 739).

Month 12 to 24: Your score continues to improve as your accounts age and your payment history lengthens. Many people reach 700+ scores by this point.

The exact timeline depends on:

- How many accounts you open

- Your payment history (perfect vs. occasional late payments)

- Your credit utilization percentage

- Whether you become an authorized user on an old account

Be patient. Building credit is a marathon, not a sprint. Consistent good behavior over 12 to 18 months builds strong credit that lasts.

Can I build credit without a credit card?

Yes, but it is harder and slower. Credit cards are the most efficient tool for building credit, but they are not the only option.

Ways to Build Credit Without a Credit Card:

Credit Builder Loans: These report to credit bureaus just like credit cards and can build payment history over 6 to 24 months.

Become an Authorized User: You can become an authorized user on someone else’s credit card without having your own card.

Rent Reporting Services: Services like Rental Kharma, RentTrack, or LevelCredit report your rent payments to credit bureaus. This can help build payment history, though not all scoring models count rent payments.

Utility and Phone Bill Reporting: Some services (like Experian Boost) allow you to add utility and phone bill payments to your credit report for a small boost.

Auto Loans or Personal Loans: If you can get approved for a small personal loan or auto loan (which is difficult with no credit), making on-time payments builds credit. However, approval is unlikely without a co-signer.

The Reality: While you can technically build credit without a credit card, the process is much slower and more limited. Secured credit cards exist specifically for people with no credit history and are designed to be easy to get approved for. If your concern is managing debt, remember that you can use a credit card responsibly by paying the full balance every month and never paying interest. The card is just a tool.

For fastest results, combine a secured credit card with a credit builder loan. This gives you both revolving credit and installment credit, creating a well-rounded credit profile.

What is the fastest way to get a credit score?

The fastest way to establish a credit score is to become an authorized user on an old, well-managed credit card account while simultaneously opening your own secured credit card.

Why This Works:

- The authorized user account gives you instant credit history (the age of that account transfers to your report)

- Your secured card creates your own independent credit account

- You start building payment history immediately

- You can have a credit score within 3 to 4 months

Step-by-Step Fast-Track Method:

Day 1: Apply for a secured credit card (approved same day)

Day 1: Ask a trusted family member with excellent credit (750+ score, 5+ years of account age, perfect payment history) to add you as an authorized user

Day 30 to 60: The authorized user account appears on your credit report, giving you years of borrowed credit history

Month 3: You make your third payment on your secured card, giving you 3 months of payment history

Month 3 to 4: Your first credit score is generated, likely in the 650 to 700 range if everything was done correctly

Important Caveats:

- This only works if the authorized user account is old and in excellent standing

- Not all credit card issuers report authorized users to all three bureaus (verify before being added)

- You still need to manage your own credit responsibly; the authorized user status is just a boost

Without Authorized User Option: If you cannot become an authorized user, opening a secured credit card and making on-time payments will get you a credit score in 3 to 6 months. It is slower but still effective.

There are no legitimate shortcuts beyond this. Anyone promising instant credit or overnight score boosts is selling a scam. Building credit takes a minimum of 3 months no matter what strategy you use.

Final Thoughts on Building Credit From Scratch

Building credit with no credit history in the USA is challenging, but it is absolutely achievable. Thousands of people successfully build credit from zero every single month using the exact strategies outlined in this guide.

The Key Principles:

- Start with a secured credit card (your foundation)

- Consider becoming an authorized user for a boost

- Use credit builder loans to diversify your credit mix

- Pay every bill on time without exception

- Keep credit utilization under 30%, ideally under 10%

- Be patient and consistent for 6 to 12 months

Your Next Steps:

- Research and apply for a secured credit card today (Discover it Secured, Capital One Platinum Secured, or Citi Secured are great options)

- Ask a trusted family member with excellent credit if they will add you as an authorized user

- Look into credit builder loans at local credit unions

- Set up autopay on all accounts

- Mark your calendar to check your credit score in 3 months

Stay Motivated: The first few months are the hardest because you are putting in effort without seeing results yet. Your credit score might not even exist for the first 3 months. But around month 4 to 6, you will start seeing real progress. By month 12, you will have good credit that opens financial doors you could not access before.

Avoid Impatience: Do not fall for “fast credit repair” scams or make impulsive decisions like applying for 10 credit cards hoping one approves you. Slow and steady wins the race. Building credit the right way takes 6 to 12 months, but the credit you build will be strong and sustainable.

The Long-Term Reward: Once you establish good credit, maintaining it is much easier than building it from scratch. You will qualify for better credit cards with rewards, get approved for auto loans and mortgages at competitive rates, rent apartments without massive deposits, and have a financial safety net when emergencies happen.

Once you start building credit, the next goal should be learning how to get a 700 credit score in 6 months in the USA.

You can do this. Start today, stay consistent, and in 12 months you will look back amazed at how far you have come.